Age: The time lived since birth. Also referred to as the Chronological Age.

Older Adults: Generally refers to individuals aged 65 and above. In some countries, the terms seniors or senior citizens are used for this demographic group. The older adult population is divided into three life-stage subgroups: the young-old (approximately 65–74), the middle-old (ages 75–84), and the old-old (over age 85).

Lifespan: The number of years someone lives from birth to death. The average lifespan for a population refers to the average Life Expectancy at Birth.

Healthspan: The number of years someone is healthy without any chronic and debilitating disease. The average healthspan for a population refers to the average Healthy Life Expectancy At Birth (HALE).

Ageing or Longevity: Generally refers to growing older and is measured as chronological age. The terms are used interchangeably on this website.

Active Ageing or Healthy Longevity: WHO defines healthy ageing as “the process of developing and maintaining the functional ability that enables wellbeing in older age.” Generally refers to growing older with good health, strength, and vitality.

Productive Ageing or Purposeful Longevity: Promotes the view that older adults can be active and purposeful contributors to their work, family, and community and engage in productive behaviors, including paid and volunteer work, continuing education, housework, and caregiving.

Population Ageing: Refers to a shift in the population demographic structure whereby the proportion of people in older age groups increases. This is driven mainly due to decline in fertility rates and an increase in longevity.

Ageing Society: Where less than 14 percent of residents are aged 65 and above.

Aged Society: Where over 14 percent of residents are aged 65 and above.

Super-aged Society: Where over 21 percent of residents are 65 and above.

Elderly Poverty: Refers to the condition where older individuals aged 65 and above are living below the poverty line.

Ageing-in-place: Refers to staying in your own home as you get older, rather than in a retirement community or a senior care facility. Seen as enabling older people to maintain independence, autonomy, and connection to social support, including friends and family.

Good Health: Refers to the state of being in good physical, mental, and cognitive health, and not merely the absence of disease or infirmity.

Physical health: State of physical well-being. It is defined as the state where an individual is able to perform the activities of daily living (ADLs) independently. ADL collectively describes fundamental skills required to independently care for oneself, such as eating, bathing, and mobility.

Mental health: Refers to psychological or emotional health. Physical health is the state of your body, while mental health is the state of your mind, feelings, and emotions. It is a state of mental well-being that enables people to cope with the stresses of life, realize their abilities, learn well and work well, and contribute to their community. Poor mental health includes mood disorders (e.g., depression or bipolar disorder), anxiety disorders, personality disorders, and psychotic disorders (e.g., schizophrenia).

Cognitive health: Refers to the health of your brain and is the state of brain functioning across cognitive, sensory, social-emotional, behavioral, and motor domains. Often described as “staying sharp” or being “right in the mind.” The four main domains of cognitive function assessment are reasoning, memory, fluency, and semantic knowledge.

Financial inclusion: Financial inclusion means that individuals and businesses have access to useful and affordable financial products and services – transactions, payments, savings, credit, and insurance – that meet their needs and are delivered in a responsible and sustainable way. [World Bank]

Financial Health: Refers to an individual’s or a household’s financial well-being and stability. It involves the ability to manage income, expenses, savings, debt, and investments effectively, as well as the capacity to withstand financial shocks or emergencies.

Financial well-being: Financial well-being is not just about avoiding financial problems but also about having the ability to recover from them. It is a new area of research and is measured in many ways, such as income stability; savings for small, unexpected expenses; savings for larger shocks like a job loss; and savings for retirement. See the next question on related metrics and measurements.

Financial security: Financial security refers to a state of being in which an individual has a stable and predictable financial situation, with sufficient resources to meet their current and future financial needs and goals.

Financial literacy: Refers to the knowledge, skills, and understanding of financial concepts and practices that enable individuals to make informed and effective decisions. It involves having a basic understanding of various financial topics, such as budgeting, saving, investing, debt management, banking, and understanding financial products and services. Financial literacy has been connected to fundamental financial behaviors such as making informed savings and borrowing decisions, investing attitudes, and behavioral intentions.

Financial Stress: Refers to the difficulty in meeting financial responsibilities due to a shortage of money. Financial stress adversely impacts physical health and psychological well-being. Studies among college students have also found that an inability to manage one’s finances can lead to a higher likelihood of financial stress among college students.

Financial well-being is a new area of research, and the definitions and measures are still evolving. Financial well-being is not just about avoiding financial problems but also about having the ability to recover from them. Many different metrics and definitions for measuring this and two of the most comprehensive ones are CFPB’s Report on Financial Well-Being in America and the US Federal Reserve’s annual Survey of Household Economics and Decisionmaking (SHED).

It would be beneficial and illuminating for other countries to follow suit with similar detailed data gathering and reporting over long periods to understand the issues and challenges, and respond by initiating policy changes accordingly.

CFPB’s Report on Financial Well-Being in America

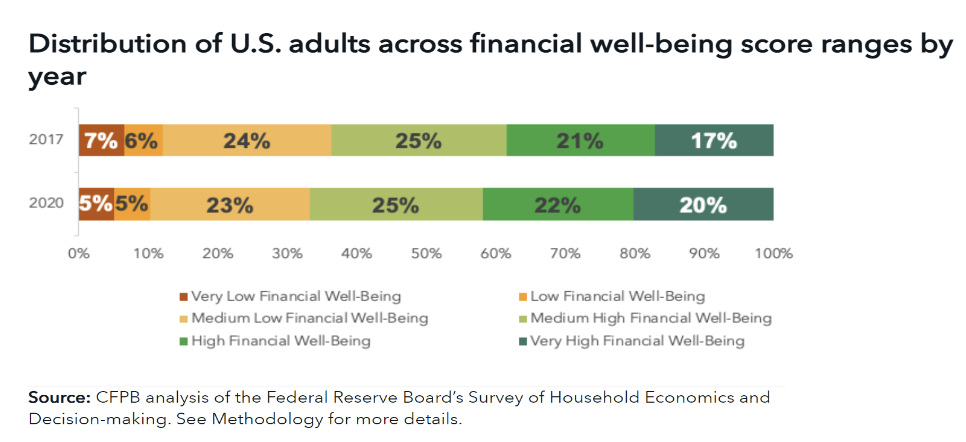

In 2017, the Consumer Financial Protection Bureau (CFPB) published its first report on Financial Well-Being in America. It measures financial well-being using a scale that was developed and tested by the Bureau in 2015 and contains 10 questions to capture how people feel about their financial security and freedom of choice. Responses are converted into an overall financial well-being “score” between 0 and 100.

![]()

A person’s financial well-being comes from their sense of financial security and freedom of choice—both in the present and when considering the future. The survey dataset includes respondents’ scores on that scale, as well as measures of individual and household characteristics that research suggests may influence adults’ financial well-being, including:

- Income and employment

- Savings and safety nets

- Past financial experiences

- Financial behaviors, skills, and attitudes

A person’s financial well-being is determined by the extent to which they feel that they:

- Have control over day-to-day, month-to-month finances

- Have the capacity to absorb a financial shock

- Are on track to meet their financial goals

- Have the financial freedom to make the choices that allow one to enjoy life

From 2017 to 2020, the average financial well-being score for American adults increased from 54 to 55. As shown in the Figure below, the percentage of adults with high or very high scores increased from 38 percent to 42 percent, while the proportion with low or very low financial well-being decreased from 13 percent to 10 percent.

This increase aligns with prior CFPB research examining the finances of Americans before and during the early months of the pandemic and suggests that the robust government response to the pandemic − including stimulus payments, expanded unemployment benefits, and mortgage and student loan forbearance − may have prevented financial difficulties for many families, despite widespread economic uncertainty and a spike in unemployment.

At the same time, 10 percent of adults still reported having low or very low levels of financial well-being. These are the individuals who experience the most severe financial and material hardships, including housing and food insecurity.

CFPB also publishes a report on the Financial Well-Being of Older Americans. The report describes the distribution of financial well-being scores for adults ages 62 and above, and the relationship between financial well-being and age. The report shows that financial well-being generally increases with age, but declines again at later ages. In addition, the report examines and quantifies the association of financial well-being with a range of topics, including employment and retirement; housing situation; debt; family and living arrangements; health-related experience; and financial knowledge, skill, and behavior.

US Federal Reserve’s Annual SHED Survey

The US Federal Reserve has been conducting a yearly survey on the ‘Economic Well-being of US Households’ since 2013. The Survey of Household Economics and Decisionmaking (SHED) evaluates the economic well-being of US households and identifies potential risks to their financial stability, taking into consideration age, occupation, duration of occupation, education, and more.

The survey includes modules on a range of topics of current relevance to financial well-being, including credit access and behaviors, savings, retirement, economic fragility, and education and student loans.

The latest report was published in May 2023 and covers the Economic Well-Being of US Households in 2022. Key findings are

- Overall financial well-being declined markedly over the prior year. Seventy-three percent of adults were doing at least okay financially in 2022, down 5 percentage points from 2021. Thirty-five percent of adults said they were worse off financially than a year earlier, the highest level since the question was first asked in 2014.

- Income variability: The mismatches between income and expenses due to income volatility can lead to financial challenges. Seventy percent of the families in the US had roughly the same income from month to month in 2022. However, it varied occasionally for 20 percent and varied quite often for just under 10 percent. Some families can easily manage this income variability, but for others, this may cause financial hardship. Income volatility also varies by industry, and workers in the hospitality and leisure industries were the most likely to have variable income. Also, many adults engage in “gig work,” or informal paid activities, often a source of volatility. In 2022, 10 percent of American adults reported they struggled to pay their bills in the past 12 months because their income varied.

- Bills and regular expenses: Eighteen percent of US households said they were unable to cover their current monthly expenses fully in 2022 and had to defer some of their housing-related bills (water, gas, electricity, rent, or mortgage) or non-housing related bills (credit cards, phone or cable bill, student loan, car or other payments). This indicates they are a modest financial setback away from hardship.

- Dealing with small, unexpected expenses: It is measured in SHED surveys as the ability to cover a hypothetical emergency expense of $400 exclusively from cash, savings, or a credit card paid off at the next statement (i.e., without borrowing or selling something). Sixty-three percent of adults said they would be able to cover the expense without borrowing or selling something. Another 24 percent said they could cover this by borrowing from someone, selling something, or revolving on a credit card, while 13 percent indicated they had no ability to find $400 in case of an emergency. This suggests that many adults in the US are living from paycheck to paycheck, unable to meet their monthly financial obligations, and any expectation of their ability to save for retirement is unrealistic.

- Financial resilience (preparedness for larger shocks): It is measured based on whether people have savings sufficient to cover ‘three months of expenses’ if they lose their primary source of income. 54 percent said they had set aside dedicated emergency savings, while 16 percent said they could cover three months of expenses by borrowing or selling assets. In total, 70 percent could tap savings or borrow or sell assets if faced with a financial setback of this magnitude, while 30 percent of adults indicated they could not cover three months of expenses by any means.

As an introduction to longevity, we highly recommend a short paper, A Prescription for Longevity in the 21st Century, by Dr. Phil Pizzo, an authority in the field. Dr. Pizzo has become a mentor and a friend over the years. He started the Distinguished Careers Institute (DCI) at Stanford University after a very distinguished career. He was the former Dean of the Stanford School of Medicine, and now in his late 70s, he is currently studying to become a rabbi, demonstrating vividly to all of us that learning has no age limits.

In this paper, Dr. Pizzo postulates that medical care and genetic predisposition constitute approximately 30 percent of the risk for early death. The remaining 70 percent is within our control and is determined by social circumstances, environmental exposure, behavior, and lifestyle.

His ‘Prescription for Longevity in the 21st Century‘ revolves around renewing purpose, building and sustaining social engagement, and embracing a positive lifestyle. The positive lifestyle choices include nutrition, exercise, and sleep.

Ageing well extends beyond physical and mental health and includes living with a sense of dignity and purpose.

In the article, Paint Your Retirement Canvas, Life Design Coach Abhi Patwardhan states that many new retirees go through phases of happiness and unhappiness, boredom and dissatisfaction. While many spend years making financial plans for retirement, the non-financial aspects get ignored. Having a sense of purpose, caring for your emotional and physical health, and having a community to support you are what will give you years of joy and fulfillment in later life.

The purpose is the most important and yet hardest to define. A highly recommended book on this topic is ‘The Path to Purpose: Helping Our Children Find Their Calling in Life‘ by Stanford Professor William Damon. He says that purpose is often conflated with words like meaning and passion but purpose is something different. It is broader than a goal and is the guiding motivation that gives your life a sense of direction. It is what makes you want to wake up in the morning. According to Damon, a life purpose has three components:

- It’s a long-term calling, act, or way of life that interests you,

- It’s something you have some competence in, and

- It makes a marginal difference in the world.

Striving to be the best parent you can is a Purpose — raising kids to become caring, respectful, and happy adults is your way of making a material impact. It’s also common to have multiple purposes in life: Your family, your community, and the satisfaction you get from your job are all common sources.

Four key areas that contribute to the length and quality of life are:

- supportive relationships

- health and wellness (exercise, nutrition, and sleep)

- financial stability and financial security

- productive and purposeful engagement.

Productive and purposeful longevity promotes the view that older adults can be active and purposeful contributors to their work, family, and community and engage in productive behaviors.

These could include paid and unpaid volunteer work, continuing education, lifelong learning, special interests, hobbies, or housework. Most of these activities have a beneficial impact on their physical and mental health.

Studies show that productive and purposeful engagement:

- has positive benefits on physical and mental health and increases longevity

- provides for additional financial security; creates continued opportunities for social engagement and participation in society

- reduces experiencing social isolation and contributes positively to life expectancy and quality of life

- contributes to the parts of life that increase longevity, such as supportive relationships, health and wellness, financial stability, and productive engagement

One of the examples of productive engagement is Experience Corps (EC) in the United States. It is a community-based volunteer program that engages people over 50 as tutors for young students to help them become better readers by the end of third grade. The program ensures volunteer success through extensive training, peer networks, and ongoing evaluation. It employs a structured, evidence-based model that improves the overall reading ability of students by building their fluency, accuracy, and comprehension skills.

The program has proven to be a “triple win,” helping students succeed, older adults thrive, and communities grow stronger. Results show that the older EC volunteers experience fewer depressive symptoms, have a better cognitive function, and have fewer declines in health. This evidence supports the social model of health promotion in that it suggests that it is not just the activity (e.g., volunteering) but the nature of the activity —social, cognitive, and/or physical engagement—that leads to positive health outcomes.

Academic references on the benefits of productive longevity for older adults

The Framework for Considering Productive Ageing and Work by Paul A. Schulte and others at the National Institute for Occupational Safety and Health, Centers for Disease Control and Prevention, Cincinnati, Ohio. The paper notes that the US population is experiencing a demographic transition resulting in an aging workforce and aims to elucidate and expand an approach to keep that workforce safe, healthy, and productive. It concludes that a productive ageing framework provides a foundational and comprehensive approach to addressing the aging workforce and involves the following elements:

- life span perspective

- comprehensive and integrated approaches to occupational safety and health

- emphasis on positive outcomes for both workers and organizations

- supportive work culture for multigenerational issues

Interdisciplinary Joint Academy Initiative on Aging in Germany: The Interdisciplinary Joint Academy Initiative on Aging published a comprehensive report in Germany titled More Years, More Life Recommendations of the Joint Academy Initiative on Ageing. The report presents a set of recommendations based on a central hypothesis: The extension of the human lifespan opens up possibilities for harnessing progress and development. With additional years of life, there are numerous avenues to explore, including individual life concepts, intergenerational coexistence, and the overall sustainability of societies.

MacArthur Research Network on Successful Aging Community Study (1988-95) finds that engagement in meaningful activities contributes to good health, cognitive performance, satisfaction with life, and longevity, as well as providing a potentially effective means of reducing costs of physical and mental illness in later life.

A few academic papers researching the economic contribution of older adults have been published in the last decade.

Academics usually talk about the first and second demographic dividends. Professor Linda Fried, Dean of the Mailman School of Public Health at Columbia University, talks about the Third Demographic Dividend. She says, “Perhaps the greatest opportunity of the twenty-first century is to envision and create a society that nurtures longer lives not only for the sake of the older generation but also for the benefit of all age groups.”

One of the most cited papers on the economic contribution of older adults is Valuing Productive Non-market Activities of Older Adults in Europe and the US. It provides a framework for measuring the economic contribution of older adults (defined as adults aged 60+) in Europe and the US. The research methodology includes examining participation in and calculating the value generated by the older adults’ market activities and productive non-market activities (PNMA). It estimated that contributions in the US and sample European countries, where older adults made up 21 percent and 14 percent of the population, respectively, added to the equivalent of 7.3 percent of gross domestic product (GDP).

The report, The Longevity Economic Outlook, by the Economist Intelligence Unit (EIU) for AARP was published in 2019 and provided an update of a 2013 AARP study on the economic contribution of the 50+ population in the US. It calculates their contribution to the US economy at USD 8.3 trillion, or 40 percent of gross domestic product, up from USD 7.1 trillion in 2013. Put another way, if America’s 50+ population were its own country, its GDP would now be the world’s third largest, following the US and China.

Another important paper is Population Aging and the Three Demographic Dividends in Asia, published by the Asian Development Bank. The study examines the structural shifts in the population’s age mix and the resulting economic growth potential. The study covered selected Asian economies – Japan, South Korea, Taiwan, and Malaysia – from 1950 to 2050 and analyzed the impact on economic growth in terms of the first and second demographic dividends.

The current work-life model follows an ‘age-segregated approach’ to life, with three distinct and sequential phases of education, work, and retirement. We typically enjoy 20-25 years of childhood and student life as young adults, followed by 30-40 years of working life as adults. Post that, we had 10-15 years of retirement as older adults , and savings from a 40-year career were generally enough to support this period, aided by government pensions in some countries and support from children in many cultures.

With an increased lifespan, we have added an extra 20-30 years. This is, of course, a cause for celebration, but we are slower to catch on to the implications of these additional years on our financial health and well-being. With the current work-life model, the extra years have extended the retirement period. It isn’t easy to sustain a 30 to 40-year retirement period with savings from a 40-year career.

We need to move away from the ‘age-segregated approach’ towards a working-life continuum or an ‘age-integrated approach,’ which suggests that life should instead be a succession of jobs, interspersed with periods of work and non-work (voluntary and involuntary) and lifelong learning.

Evolving Nature of Jobs and Reskilling and Upskilling: The future of work and the future of jobs is evolving rapidly, with the advent of technology, increasing automation, and globalization. The World Economic Forum (WEF) report, An Aging Workforce isn’t a Burden, it’s an Opportunity, states that most individuals are likely to change jobs at least twice in their working lives, voluntarily or involuntarily.

As per Bloomberg’s Countries with the Longest, and Shortest Retirements, this means at least three distinct employers for an individual before the average career ends at 65. The shift requires a mindset of lifelong learning, with periods of reskilling and upskilling. Therefore, corporations must consistently invest in employee training and engagement throughout their careers, not just for the typical onboarding.

Building Resilience and Failure Immunity: The transition between periods of work and non-work (voluntary and involuntary) means younger adults need to join the workforce with a new mindset. The individuals also need to have the mental resilience and failure immunity to manage such transitions, especially if these are involuntary in nature.

Many adults may not want to discuss financial insecurities around retirement. Still, something as simple as a short workshop on financial well-being and longevity can put more significant changes in motion. By bringing attention to the issue proactively and professionally, you can ensure that you don’t fall into the trap of ageism or age-related myths and biases.

Companies such as Walmart are helping mid-career employees manage their careers by offering “Design Your Career” workshops. Walmart Global Tech, the IT division of Walmart, partnered with Alt-Lyf to conduct webinars and workshops in 2021 and 2022 for over 500 employees in India. See details under Useful References.

Designing for a 100-Year Life (Workshops and training programs): Bringing attention and awareness to the challenges proactively and professionally can ensure you are well-prepared for retirement. One of the best workshops for “Designing Your Life” is offered by Professors Bill Burnett and Dave Evans of Stanford University. You can start by reading their book Designing Your Work Life. They have also trained and certified coaches worldwide to promote the Designing Your Life philosophy to tackle the difficult transition points in life.

In Singapore, two courses are offered by NUS-SCALE (the Continuing Education arm of the National University of Singapore). Recognizing the importance of such a program, the Singapore government has approved the courses under its SkillsFuture program, thereby heavily subsidizing the course fees for Singapore residents. See additional details in Singapore: Designing for a 100-Year Life (NUS-SCALE).

Free online courses: Alt-Lyf offers some free online self-learning programs for individuals interested in learning independently.

Global average life expectancy is projected to reach 77.2 by 2050 (versus 48 in 1950).

Between 2015 and 2050, the proportion of the world population over 60 years old will nearly double, from 12 percent to 22 percent.

By 2030, the population of those aged 60+ is expected to grow by 56 percent, from 962 million (2017) to 1.4 billion. This number should reach nearly 2.1 billion by 2050.

Globally, the number of older persons is growing faster than those in all younger age groups. By 2030, older persons will outnumber children under 10 (1.41 billion versus 1.35 billion). By 2050, there will be more people aged 60 years or over than adolescents and youth aged 10-24 years.

In most countries, the proportion of older people in the population will increase to 20 percent of the respective population by 2050.

Women tend to live longer than men and account for 54 percent of the global population aged 60 and above, and 61 percent of the global population aged 80 and above.

Life expectancy at birth is now over 80 in 33 countries. Globally, the average lifespan has risen by 6 years between 2000 and 2019, from 66.8 to 73.4 years.

The maximum human lifespan so far is capped at 122 years. The current longevity record is 122 years and five months, held by French Jeanne Calment, who passed away in 1997.

In the US, the entire ‘Baby Boomer’ population, as well as a majority of the ‘Boomer II’ or ‘Generation Jones’ generation, is over 60 years old.

Life expectancy in the U.S. exceeds the global average, at just above 79 years. In 1900, it was just over 47 years. The extra decades came courtesy of vaccines, antibiotics, sanitation, and improved detection and treatment of a range of diseases. Advances in genetics and in our understanding of dementia are helping to extend longevity.

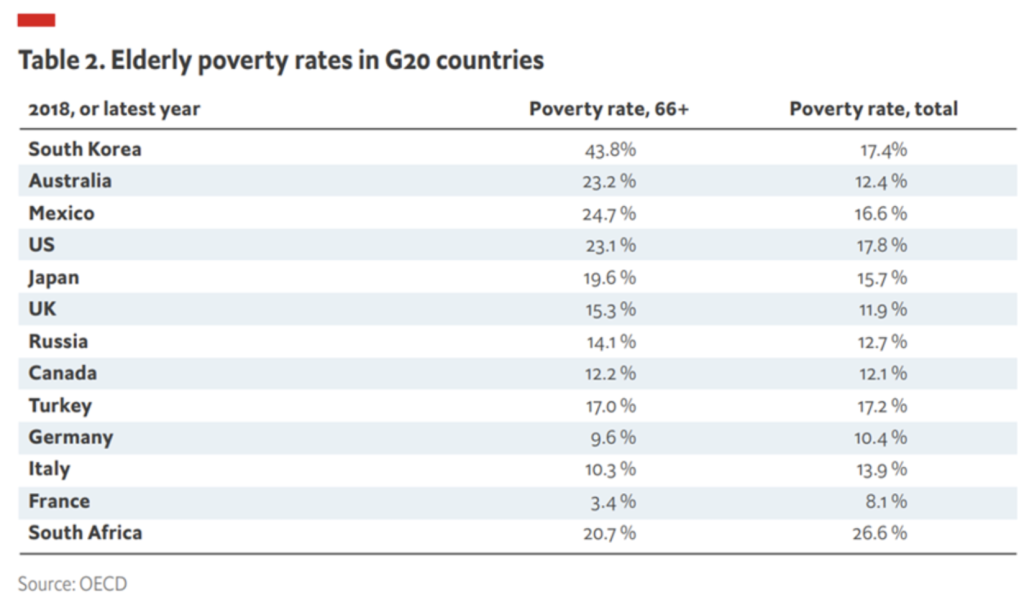

Senior poverty refers to the percentage of older adults living below the poverty line.

The Economist Intelligence Unit (EIU) published a report in 2020 titled “Shifting Demographics: A global study on creating inclusive environments for ageing populations,“ and the results are daunting. For example, in South Korea, 43.8 percent of adults aged 66 and above are living below the poverty line. That means nearly half of South Korea’s senior citizens struggle to get by.

In the United States and in Australia, over 23 percent of the people in the corresponding age group live below the poverty line. The table below shows that these percentages for older adults are significantly higher than the national poverty rates.

Figure 1, Source: The Economist, May 2020

Anju Patwardhan wrote a LinkedIn post on this topic in 2022.

Squid Game, a popular Korean TV show, illustrates the issue well. The Korean TV series made history in 2022, winning six Emmy awards. The survivalist drama is about a competition among 456 indebted participants pitted against one another for a cash prize of $40 million. Losers face instant death.

In his acceptance speech, the leading man and best actor winner, Lee Jung-Jae, said that the show made “realistic problems we all face come to life.” Obliquely, he was referring to the extreme steps people will take to alleviate poverty. Even though the show’s premise is fictional, the problem is real, and it is much worse for older adults in the 65+ age group, as seen in the EIU data.

The senior poverty numbers for the Nordics and countries like France and Germany are lower and potentially reflect the strong social support systems.

Singapore and Japan have the fastest ageing populations in the world, and the financial well-being of older adults will be a massive challenge unless structural changes continue to be made to provide ongoing support to an increasing percentage of older adults.

In most countries, the policies mandating retirement age have not kept pace with the increased lifespan, and people continue to retire between the age of 60 to 65. It is not easy to support a 30 or 40-year retirement with savings from a 40-year career. This has resulted in financial insecurity among potential retirees. In addition, the widespread issue of inadequate or nonexistent pension schemes in many countries has compounded the problem.

Addressing senior poverty and ensuring the financial well-being of older adults is critical. Some older adults elect to work longer, while others have no choice but to support themselves and their families. While many older adults may want to continue working full-time, part-time, or in flexible jobs to support themselves financially, age discrimination in the job market and the bias against older workers add to the struggle to find a source of income in later life.

To ensure financial health and security, more must be done to reduce ageism at work and provide age-appropriate economic opportunities.

Studies show that financially literate individuals are better equipped to manage their everyday finances, are more resilient to temporary economic shocks, and are better prepared for their future financial needs over the course of their lifetime.

Some studies have found that financial knowledge is associated with financial well-being. Also worth reading are the papers Economic Literacy: An International Comparison and Financial Literacy and Preparation for Retirement.

A paper was published in early 2023 on the association between financial literacy and financial well-being when mediated by financial stress. The paper Financial Well-Being in the United States: The Roles of Financial Literacy and Financial Stress examines the role of financial stress in explaining the relationship between financial literacy and financial well-being among individuals in the United States. It concludes that financial literacy was positively associated with financial well-being. The study also found that the association between financial literacy and financial well-being was mediated by perceived financial stress experienced by individuals. Financial education was positively associated with financial literacy in this study.

The broader implications of the findings of these studies for individuals’ sustainable financial well-being are relevant for policymakers, financial educators, financial counselors, and financial planners.

Studies show that financial insecurity or poor financial health adversely impacts physical and mental health. Financial insecurity and stress impact people beyond their physical health and are associated with depression, anxiety, and a loss of personal control.

Studies among college students have also found that an inability to manage one’s finances can lead to a higher likelihood of financial stress among students.

Globally the COVID-19 pandemic demonstrated this correlation. The paper COVID-19 Financial Stress and Well-Being in Families examines the financial and social impact of COVID-19 on families and their well-being. The study finds that the pandemic caused varying degrees of financial stress in families, along with feelings of fear and demotivation due to the general lockdown.

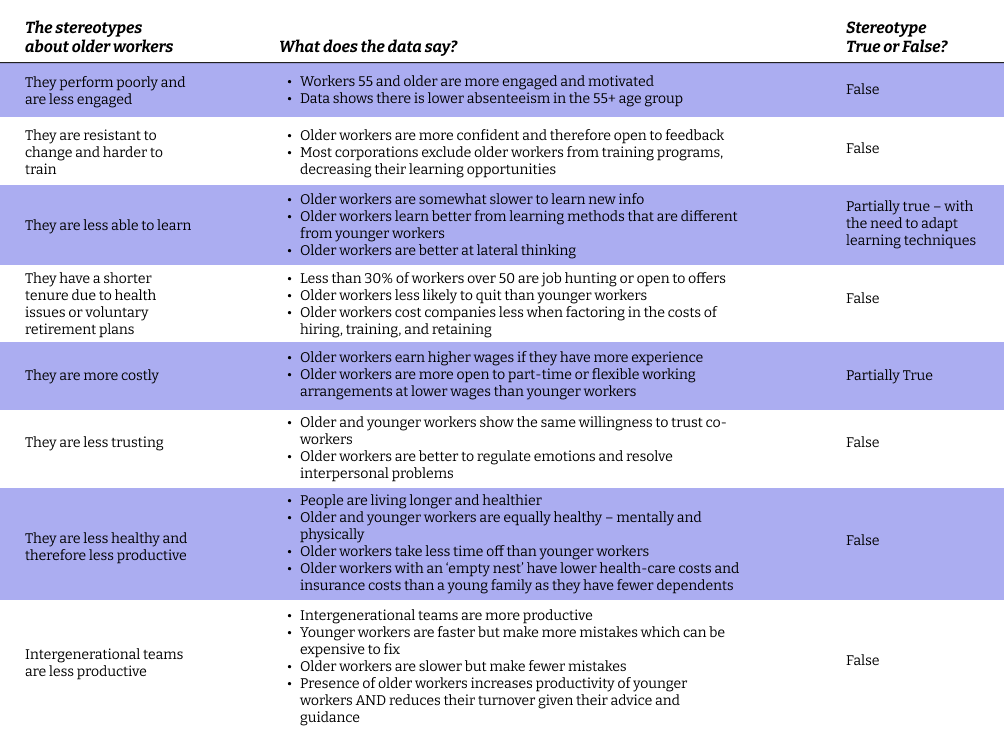

Ageism and age-related biases are a problem in most companies. So what is real, and what is a corporate myth?

Chip Conley’s book Wisdom@Work: The Making of a Modern Elder has an entire chapter dedicated to ‘debunking ageist stereotypes.’ I have attempted to summarize the key points below but have probably not done justice to the significant contributions by Richard Posthuma, Michael Campion, and others to Chip’s book. I highly recommend reading the book, or at least Chapter 9, to understand this better.

As a corporate leader, you can rely on this research, although it is US-centric, and try to minimize the biases in your company. If you are not in the US, you can rely on this research or maybe help by commissioning similar studies in your markets to debunk the myths. At a minimum, you can influence hiring within your team and promote age diversity and intergenerational engagement.

Studies have shown that intergenerational teams perform the same or better than teams consisting of only young adults or only older adults. An interesting study was conducted at Mercedes Benz’s large truck assembly plant in Germany. Compared to many service-sector jobs, productivity in this plant requires more physical strength, dexterity, agility, etc. (which tend to decline with age) than experience and knowledge of human nature (which tend to increase with age).

The results published in Productivity and Age: Evidence from work teams at the assembly line are fascinating. This research shows that even in an environment requiring substantial physical strength, the joint productivity of teams does not decline for workers between 25 and 65 years of age. The decline in some characteristics with age is compensated by other characteristics that increase with age, such as experience and the ability to operate well in a team when tense situations occur, typically when things go wrong, and there is little time to fix them. As a result, mixed-age teams make fewer production errors, while performing at the same levels of productivity.

For decades, academic and policy debates in high-income countries (HICs) emphasized the negative consequences of work on ageing (stress, physical exhaustion, worsening health) and neglected the positive effects. Consistent with this one-sided narrative, ‘protecting’ people from work through policy measures such as mandatory retirement age, fewer weekly working hours, or other measures has been considered a major societal achievement of the past century.

As we have moved from an agrarian to an industrial to a knowledge/service economy, the debate needs to evolve. Recent evidence from HICs demonstrates the positive outcomes of work on health in later life. This includes physical, mental, and cognitive benefits [MacArthur Research Network].

Rather than eliminating exposure to work in later life, these studies suggest that older adults benefit from a phased transition from full-time to part-time or flexi-time jobs.

A study, A Global View on the Effect on Health of Work Later in Life, by Professor Ursula Staudinger from Columbia University, inspects labor force participation and evidence showing that working until later in life has positive physical, mental, and brain health impacts. Given the increasing longevity of individuals, it is crucial to rethink the role of work to ensure both macroeconomic and microeconomic benefits, as well as to maintain the physical, mental, and cognitive health of aging individuals. This particularly applies to lower-skilled work, which requires redesigning to enable longer and more satisfying work lives.

Collecting data on productivity and disability trends across different occupations is essential for suggesting timely task modifications. Apart from physical and mental strain, attention must be given to job stress when optimizing extended work lives. Governments and employers should prioritize workplace policies and practices that support productivity and well-being for workers of all ages.

It is important for people to recognize the realities of longer lives and plan accordingly for all stages of life. To achieve this, various sectors such as education, work, health, and social services need to play a role in this significant undertaking.

Additional studies need to be conducted across industries to review evidence on the association between work (white collar jobs) and its impact on an individual’s physical, mental, and cognitive health in later life. Nevertheless, an impressive and growing body of evidence suggests productive and purposeful engagement is health-promoting and economically beneficial – creating continued opportunities for social engagement and participation in society and increased financial security.

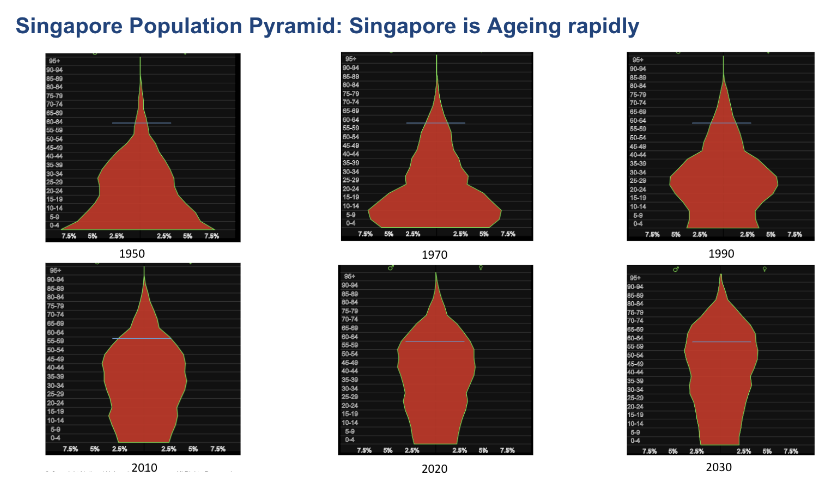

Singapore’s population is ageing rapidly.

In 2019, Singapore transitioned from an ‘ageing’ society to an ‘aged’ one.

By 2030, it will be a ‘super-aged’ society.

By 2030, over 900,000 residents will be aged 65 and above (1-in-4 or 25 percent of the total resident population).

The average life expectancy in Singapore is 83.6 years, making 50 the mid-point of one’s adult life.

Life expectancy at age 65 is 21.3 years in Singapore, up from 8.5 years in 1975.

Over 89 percent of Singapore residents are homeowners. This is a strong factor in retirement adequacy and in supporting ageing-in-place. While Singaporeans may be asset-rich, they also tend to be cash-poor and are not financially ready for a long time.

Prudential Singapore, an insurance company, partnered with the Economist Intelligence Unit to conduct a series of studies in 2018-19. One of the reports titled Ready for 100, Preparing for Longevity in Singapore focuses on challenges related to longevity in a small country with a prosperous economy and a rapidly ageing population.

As of 2022, the Labour Force Participation Rate (LFPR) for the 65 and above age group in Singapore is 32.1 percent (OECD 2022 average is 16.7 percent), with financial necessity as the primary reason to remain productively active.

Over half the people interviewed in the 62+ age group (52 percent) said they planned to continue relying on a salary to support themselves. This expected reliance on a salary after age 62 indicates a future tension in the residents’ ability to provide for themselves to age 100.

The Singapore government is exceptionally forward-thinking and has launched multiple initiatives to promote healthy and productive longevity. For example, Singapore began the Action Plan for Successful Ageing in 2015. This research was to determine how to prepare citizens for longevity in terms of health, happiness, social support, work, and the corporate world. The Action Plan for Successful Ageing 2023 report outlines progress in preventive health measures and breaks down their approach to action – Care, Contribute, and Connect.

Financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit, and insurance – delivered in a responsible and sustainable way. [World Bank].

The World Bank Findex measures financial inclusion as having an account at a bank or regulated institution such as a credit union, microfinance institution, post office, or mobile money service provider. Based on this definition, in 2021, 76 percent of all adults globally were financially included. While this is a significant improvement from 51 percent in 2011, it shows that 24 percent of all adults globally, or 1.4 billion individuals, were still financially excluded in 2021 and lacked access to basic financial services [World Bank Findex]. Another 45 percent had basic accounts but did not have access to diversified investment and savings options, low-cost payment systems, core household and business insurance, or credit.

Greater financial inclusion is one of the key priorities of the United Nations’ Sustainable Development Goals (SDG), as it enables households and informal economies to increase resilience and capture economic opportunities and is referred to in SDG 10 (Reduce inequality within and among countries) and several other SDGs.

The G20 has pledged to promote financial inclusion globally and uphold the G20 High-Level Principles for Digital Financial Inclusion. Additionally, the World Bank Group views financial inclusion as a crucial facilitator in reducing extreme poverty and fostering shared prosperity. This is also relevant for older adults as they may experience unequal access to certain services and transactions in our ‘digital age,’ or they may not be able to afford these services post-retirement due to their financial situation.

The World Bank has identified 5 Pillars of Financial Inclusion around which measures and efforts have been organized to improve the state of things around the world. In a sense, these also act as benchmarks for measurement:

Pillar 1: National Financial Inclusion & Fintech Policy and Strategy

This pillar focuses on providing comprehensive strategies and assessments for financial inclusion, with an increasing emphasis on digital financial inclusion and leveraging fintech. It includes activities such as conducting assessments of access to finance, sustainability of providers, and national policies. It also involves assisting in the design and implementation of national or subnational roadmaps and action plans to achieve financial inclusion objectives.

Pillar 2: Financial Products and Providers for Underserved Segments

Pillar 2 aims to support policy reforms specific to financial products and providers that cater to underserved segments, including women and rural populations. It involves offering technical assistance to expand the range of appropriate products and services for underserved individuals and micro, small, and medium-sized enterprises (MSMEs). Additionally, it focuses on enabling the entry and operation of innovative providers and strengthening competition to enhance access and ensure a level playing field.

Pillar 3: Financial Consumer Protection

Financial consumer protection is crucial for ensuring that financial inclusion benefits consumers without exposing them to potential harm. This pillar provides technical assistance in various aspects of consumer protection, including market conduct supervision, disclosure and transparency, fair treatment and business conduct regulation, and accessible and effective channels for alternative dispute resolution. It also addresses data privacy and protection issues in the context of fintech and digital financial services.

Pillar 4: Financial Capability and Behavioral Insights

Financial capability refers to individuals’ capacity to act in their financial interest. This pillar leverages research on financial capability and behavioral economics to provide strategic advice on incorporating financial education messages into existing programs, interventions, and policies. It supports national authorities in developing a strategic approach to financial capability and utilizing behavioral insights to enhance the effectiveness of financial inclusion efforts.

Pillar 5: Micro, Small, and Medium Enterprise (MSME) Finance

This pillar focuses on providing policymakers with tools and technical assistance to monitor and analyze the supply of credit to MSMEs. It aims to identify market gaps, risks, and areas for improvement in MSME finance through systematic diagnostics. By conducting comprehensive assessments, policymakers can communicate the results to relevant stakeholders and implement measures to address identified challenges.

In addition to these pillars, the World Bank Group also works on payments and payment systems to further financial inclusion, including modernizing retail payment systems, digitizing government payments, and reforming national payment systems and remittance markets. Financial inclusion efforts are integrated into other development areas, such as support for women entrepreneurs, digital economy initiatives, and initiatives focused on women’s financial inclusion. The World Bank Group also engages with standard-setting bodies and participates in global partnerships for financial inclusion, such as the G20 Global Partnership for Financial Inclusion (GPFI) and the Payment Aspects of Financial Inclusion (PAFI) initiative.

More information and data can be found in the WBFindex report, Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19.

Loneliness refers to feelings of social isolation and disconnectedness that reflect discontent with the quality of social interaction. It is very distinct from being alone.

A study, Social isolation, loneliness and their relationships with depressive symptoms, conducted in Singapore found a significant overlap between loneliness and social isolation. It shows that 33 percent of individuals living with spouses and children still feel lonely (i.e., have no meaningful social connections). Social isolation in terms of weak connectedness with relatives and friends and loneliness were associated with depressive symptoms even after controlling for age, gender, employment status, and other covariates.

In 2017, a British commission found that nearly nine million people in the country either often, or always, feel loneliness — a condition that can have harmful health repercussions. To address this issue of loneliness and social isolation, the UK government established the position of Minister for Loneliness in 2018. The ministerial appointment was in response to a recommendation made by the Jo Cox Commission on Loneliness, which highlighted the negative impacts of loneliness on individuals’ health and well-being. These negative impacts were exacerbated for the wider population during COVID-19 but were especially relevant for older adults beyond the age of retirement.

This Time article noted that nearly 200,000 elderly across the United Kingdom hadn’t had a conversation with a friend or relative in over a month.

The UK Minister for Loneliness is responsible for coordinating efforts across various departments to tackle loneliness, raise awareness, and develop strategies to combat social isolation. The role involves working with charities, community organizations, and government bodies to address the causes and consequences of loneliness, as well as finding ways to enhance social connections and support networks.

An Indian startup – Goodfellows – was launched in 2022 to address the issue of loneliness among older adults. Over 15 million seniors in India live by themselves. While they may have found ways to fulfill their utility needs, they often lead isolated lives.

Goodfellows aims to provide companionship services for seniors through intergenerational engagement with young adults. The company uses psychometric testing to select young graduates and professionals based on their empathy and emotional intelligence and pairs them with seniors.

The services offered include assisting the elders with day-to-day tasks such as going for walks, grocery shopping, accompanying them to the doctor’s office, teaching them about technology to be able to connect with family members in other cities or countries, helping with paperwork, just chit chat or watching movies together, and more. The objective is to provide not just a service, but rather, a meaningful experience for “our beloved Grandpals” in the same way they would have experienced with their grandkids. The company also organizes collective events, learning sessions, and festival celebrations to bring the community together.

Ratan Tata, a well-known Indian industrialist and philanthropist, and the Chairman Emeritus of Tata Sons, provided seed funding for the platform. He said that “You don’t know what it means to be lonely until you spend time alone, wishing for companionship,” and emphasized how this is a growing issue in the country as more children go abroad.

You can watch a video of Ratan Tata speaking on the subject of loneliness here.

As the world population is getting older, it is important to understand the perspective of older adults as employees

- 50+ people need to work (for financial well-being),

- 50+ people can work (increasing lifespan and healthspan), and

- 50+ people want to work (physical and mental health benefits)

But most 50+ people are facing reduced work opportunities in the marketplace and are facing ageism at work.

The most difficult life stage transition for people who have worked throughout their adult lives is moving from full-time work until the retirement date to not knowing what to do the next day. A phased retirement approach enables older adults to transition gradually from full-time roles until their sixties to full retirement in the late seventies. As they get into their sixties, older adults are interested in a phased transition from full-time roles to part-time or flexible roles. They often look for flexible work arrangements closer to home.

For creating such flexible or part-time jobs for older adults, the responsibility extends beyond corporations to governmental bodies working with companies to create such jobs and formulate appropriate policies. It would significantly benefit employees and employers if companies could change how older people are employed.

A survey was conducted in Japan in 2017 to understand the employment needs and behaviors of older adults, and the results are tabulated here.

Some criteria related to the employability of older workers that need to be considered are:

- Duration: Maybe 2-5 hours per day for 3-5 days per week

- Distance: Short commute, or work from home on phone/video

- Type of Work: Light physical activity and greater opportunities for social interaction and inter-generational engagement

- Compensation: Based on interest and financial needs, it can be paid work, paid or unpaid volunteering work, learning or mentoring opportunities, etc

Additional studies must be conducted to determine the kind of employment opportunities most suited for older adults of different age groups.